Magic Quadrant for Customer Data Platforms 2026 — Gartner

Source: https://www.gartner.com/doc/reprints?id=1-2MRJYIYN&ct=260123&st=sb Licensed for distribution

26 January 2026- ID G00836173- 59 min read

By Lizzy Foo Kune, Rachel Dooley, and 3 more

The customer data platform market is bifurcating into platformization and agentification. Buyers should assess their needs for orchestration or autonomy, prioritize warehouse-native and composable architectures, evaluate cost-to-value and invest in agentic AI and automation.

Market Definition/Description

Customer data platforms (CDPs) are software applications that support customer experience use cases by unifying a company’s customer data from marketing, sales, service, commerce and other sources. CDPs unify customer data to facilitate its output to coordinate profiles between cross-functional systems, create segments and/or audience targets, optimize offers and/or decisions, and inform analysis while distributing insights that create triggers for other experiences.

Today’s CDP technology is an enterprise data strategy and technology decision: enterprise IT organizations view the investment as an essential component for both upstream technical users and downstream business users. As such, the purpose of a CDP has evolved.

Traditionally, its focus is to centralize data collection and unify customer data from disparate sources into profiles, improving contextual experiences across customer-facing functions. But today’s buying groups are cross-functional and responsible for a variety of engagement touchpoints across the customer life cycle. The 2025 Gartner Business Buyer Survey reveals that an average of two to three functional groups typically contribute requirements and objectives for a CDP purchase.1 These groups include functions such as central IT, sales, marketing, supply chain management, finance, customer service and even HR. In light of that, the purpose of CDPs is bifurcating: business users either adopt CDPs to innovate and attempt to evolve their work with limited IT support or to collaborate with enterprise data functions and elevate the role of customer data.

The CDP is not yet a substitute for an enterprise’s master data management, but it can ensure that customer profile data, transactional events and analytic attributes are available to customer-facing functions for coordinating interactions. CDPs govern the bidirectional flow of data between the front office and back office, such as go-to-market (GTM) and R&D/operations.

Nontechnical users look to CDPs to orchestrate a variety of business applications (such as marketing, sales, service, support, commerce), CRM systems, and cloud data warehouses. The goal of nontechnical users is to better coordinate GTM execution (such as unified commercial motions for B2B and customer journey orchestration for B2C business). While many of these systems also manage customer-level data and audiences for targeting, they do so in a way that makes both data governance and orchestration across channels — and across competitive vendor solutions — a challenge. CDPs aim to address this challenge by collecting and unifying disparate customer data in a centralized location, making it accessible to customer-facing teams engaging across the customer life cycle.

Mandatory Features

At a minimum, CDPs must perform:

-

Data collection**:** Ingest (extract) first-party, individual-level customer data from multiple sources and formats, online and offline, in real time and without limits on storage. This includes enterprise data sources (such as cloud data warehouses and datalakes) and data sources from business functions. Data persists as long as needed for processing and is typically left unchanged in its original source. This includes both anonymous and known first-party identifiers, behaviors and attributes.

-

Customer data object management**:** The creation and management of unified customer profiles from person-level data by integrating multiple sources using deterministic or probabilistic identity resolution. It also governs and activates related objects linked to profiles, such as audiences, campaigns, scores and accounts.

-

Activation: The ability to send segments, with instructions for activating them, to engagement tools and platforms, including those for email campaigns, mobile messaging and advertising, among others. CDPs increasingly function as centralized decision-making tools, supporting real-time personalization and next-best-action decision making.

-

Analytic reporting**:** Performance and propensity analysis for various levels of customer data, such as the attribute level, profile level or segment level.

Common Features

Common features include:

-

Segmentation:

-

An interface that enables the marketer to create and manage segments or audiences. Basic offerings support rule-based segment creation.

-

Analytic support to detect, prioritize and predict optimal responses to significant events affecting a customer relationship. Some CDPs may offer augmented segmentation, deploying AI to streamline the user workflow for this.

-

-

Integrations**:**

-

The ability to connect to and exchange data or instructions (often via out-of-the-box connectors or APIs) with other tools, programs, apps and channels. This includes first-, second- and third-party data.

-

Connections to customer experience (CX) channels and systems to collect and disseminate customer attributes and marketing engagements across customer service/support, digital commerce, sales, and other customer engagement technologies.

-

-

Data i****nteroperability:

-

Enablement of direct retrieval or querying of data from cloud-based data warehouses and the orchestration of that data to point solutions: CDPs increasingly support composable, enterprisewide data fabrics through zero-copy integrations with platforms like Snowflake and Google Cloud Platform. They expose metadata for data discovery and lineage.

-

Data model management: CDPs must create a representation of how customer data is structured, including which attributes and dimensions to include in a profile.

-

Emerging architectural models (such as data lakehouses and open table formats), which support the persistence and retrieval of structured, semistructured and unstructured data.

-

CDPs participate in data fabrics to streamline enterprisewide access and discovery of customer data, often using data virtualization. By publishing metadata through catalogs and knowledge graphs, CDPs enable other systems and AI/ML tools to discover and integrate trusted data. CDPs also capture usage insights as active metadata to enhance governance, efficiency and compliance in federated data environments.

-

-

Decisioning and data orchestration**:**

- The ability to enable automated or real-time decisioning and activation of the CDPs’ objects and their attributes across multiple sources and systems. This may include out-of-the-box models (such as next-best-action capability and channel-agnostic recommendation engines) and content/offer optimization.

-

Privacy:

- The ability to protect and audit user-level data access, mask data, use other approaches to minimize inadvertent data sharing, comply with regulatory requirements (such as General Data Protection Regulation [GDPR] and California Consumer Privacy Act [CCPA]), and synchronize individual-level consent flags.

-

Consent and preference management:

- The collection and consolidation of end-user choices and preferences regarding how their personal data should be handled, and synchronizing these choices across marketing systems and channels.

-

Experimentation and data science:

-

This includes features beyond out-of-the-box predictive models, such as the ability to import and manage machine learning models within the CDP using R or Python.

-

Additionally, CDPs may enable A/B and multivariate tests that monitor and self-optimize the customer experience based on the winning treatment.

-

-

B2B data object management**:**

- This capability supports the creation, management and governance of B2B-specific data objects, such as accounts, buying groups, opportunities, contacts and hierarchies. It governs and activates B2B objects to ensure accurate targeting, compliance and orchestration of complex B2B engagement strategies.

-

Data c****ollaboration:

- Tracking and identifying pseudonymous web visits using partnerships with identity resolution partners (such as Merkle or LiveRamp), or supporting advertising measurement and activation use cases through data clean rooms.

-

Agentic p****rocess o****ptimization:

- Packaged AI agents tailored for specific business functions that have been granted rights by the organization to act on its behalf to autonomously make decisions and take action. Examples may include data quality, audience management and journey optimization agents. Agents are dedicated to augmenting, if not automating, some of the work of the CDP — allowing it to be more efficient and effective. Advanced capabilities include the ability for CDP users to create their own agents and integrations with other large language models (LLMs) and agent platforms through Model Context Protocol.

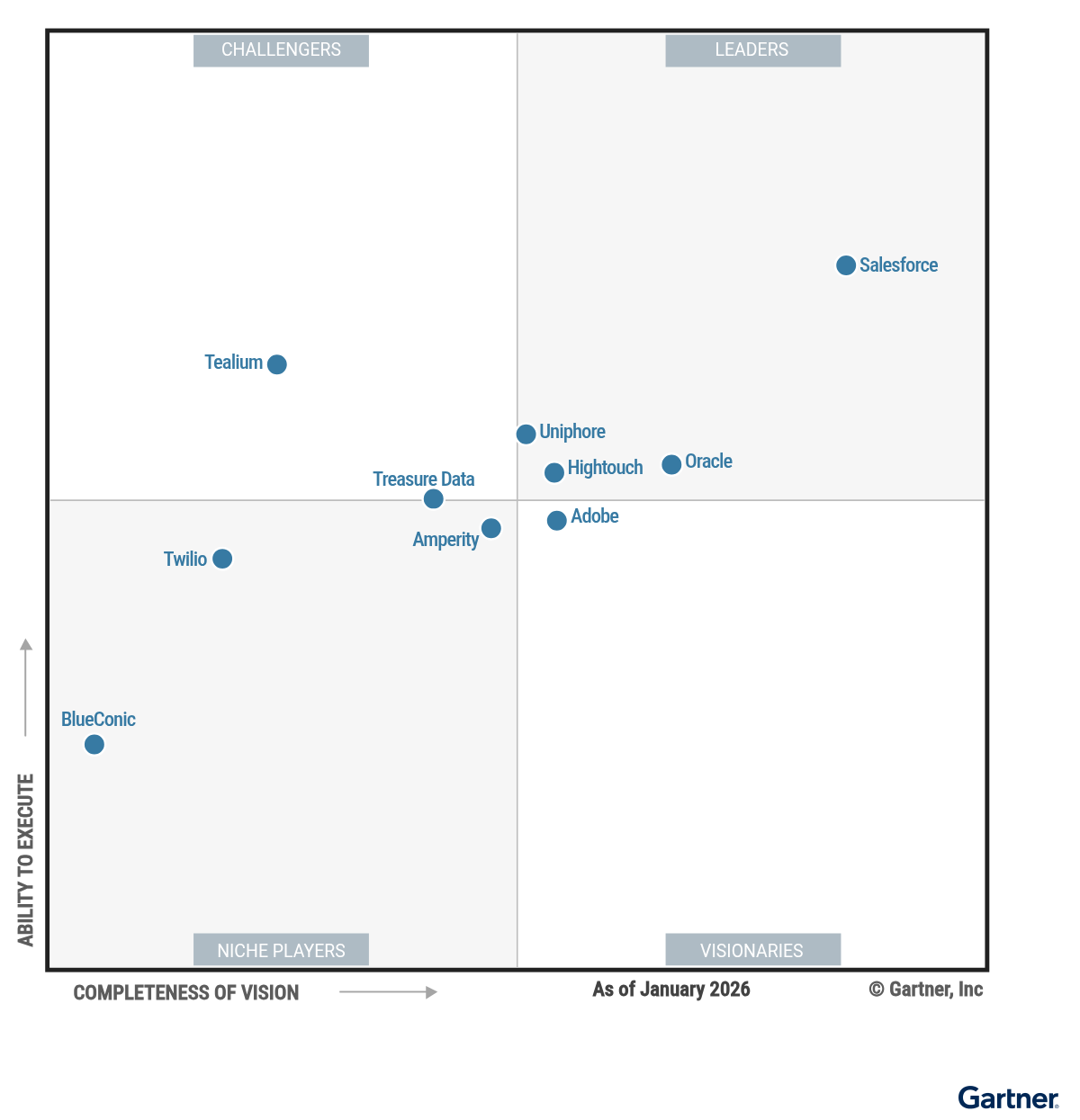

Magic Quadrant

Figure 1: Magic Quadrant for Customer Data Platforms

Vendor Strengths and Cautions

Adobe

Adobe is positioned as a Visionary in this Magic Quadrant. Its Adobe Real-Time Customer Data Platform (CDP), built on the Adobe Experience Platform (AEP), creates unified, real-time consumer and account profiles to activate insights across Adobe and external channels. Available in B2B, B2C and hybrid editions, Adobe primarily serves global B2C organizations, with a strong presence in retail, financial services and media.

In 2025, Adobe launched Adobe Real-Time CDP Collaboration for privacy-centric audience discovery between advertisers and publishers and introduced Adobe LLM Optimizer and, notably, Adobe Audience Agent for segmentation. The roadmap prioritizes full journey marketing, expanded data composability and embedding AI assistants and agents into AEP.

Adobe declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

Strengths

-

Real-time data management: Adobe differentiates with a distributed edge network that enables sub-200 millisecond decisions for in-the-moment personalization. Marketers can leverage real-time data streams to update unified profiles and instantly activate segments across Adobe and external channels.

-

Privacy and data collaboration: Adobe’s patented Data Usage Label Enforcement framework governs data usage at the attribute level. Real-Time CDP Collaboration adds a clean-room application, enabling advertisers and publishers to discover, plan and measure audiences securely — without moving data or exposing personally identifiable information (PII), addressing first-party data collaboration needs.

-

Vertical enablement: Adobe supports complex global enterprises with out-of-the-box data models and schemas for industries such as retail, financial services, healthcare and hospitality. Industry-specific use case playbooks and guided, in-product workflows help teams execute preconfigured strategies and reduce implementation complexity.

Cautions

-

Strategic alignment: Real-Time CDP excels in marketing activation and personalization, but it may not address broader enterprise data management needs. IT and data operations leaders seeking capabilities such as cross-domain data governance, data virtualization and orchestration across nonmarketing systems should carefully assess whether Adobe’s product strategy aligns with their comprehensive enterprise data management requirements.

-

Platform packaging and total cost of ownership (TCO): Adobe’s packaging may require purchasing adjacent products (e.g., Adobe Journey Optimizer, Adobe Customer Journey Analytics) to access orchestration or reporting capabilities core to other CDPs. Real-Time CDP alone is often just a starting point for business value.

-

Composability maturity: Despite the 2024 release of AEP Federated Audience Composition, Adobe’s composability and warehouse interoperability are less mature than required for current market demands. Licensing requirements for federated features may limit the economic benefits of a zero-copy architecture, reducing appeal for buyers seeking flexible solutions.

Amperity

Amperity is positioned as a Niche Player in this Magic Quadrant. Its solution, Customer Data Cloud, focuses on solving complex identity resolution challenges via AI and machine learning (ML) and enables composable data management through a Lakehouse CDP architecture. The company’s operations are focused in North America, and its clients generally tend to be large B2C enterprises across sectors such as retail, travel and financial services.

Future plans include investments in “bring your own architecture” capabilities, such as bring your own compute; its generative AI (GenAI) tool, AmpAI; and expanded zero-copy data sharing for cloud data warehouses.

Strengths

-

Customer profile unification**:** Amperity’s patented Stitch technology leverages up to 45 AI models to resolve complex identity challenges without requiring rigid schemas. Large enterprises with complex or messy, unstructured data can confidently activate their campaign strategies and achieve greater relevance from higher match accuracy that is independent of third-party data providers.

-

AI vision: Amperity integrates GenAI throughout its platform, using agents for identity resolution and segment development based on natural language. In 2025, it released Chuck Data, an AI-native terminal assistant that enables data engineers to simplify customer data model management, increasing accuracy and significantly reducing coding time.

-

Cohesive ecosystem: Amperity now supports a “bring your own architecture” that separates compute and storage. In addition to a Lakehouse CDP for zero-copy data sharing with major cloud data warehouses, such as Databricks and Snowflake, clients are able to run queries on their own cloud computing layer and execute predictions and actions using their own AI models.

Cautions

-

Business viability and pricing model transition**:** Amperity’s net revenue retention lags peers, and its business faces uncertain impact of a strategic pivot to consumption-based pricing. As clients transition to the new model, they will need to recalculate how their ongoing use cases consume Amps. The potential volatility of billing based on credit consumption may shift the cost-to-value calculation of a client’s investment in the CDP and exacerbate revenue retention challenges if investment cases weaken.

-

Decisioning and data orchestration: The platform trails other vendors in this Magic Quadrant in decisioning and data orchestration capabilities, reducing its appeal for brands seeking native, advanced orchestration. Amperity relies on custom implementations for critical features, such as algorithmic attribution modeling, and the platform possesses limited out-of-the-box performance alerts for triggers, requiring clients to invest in additional customization or external tools.

-

Limited B2B vision**:** Amperity’s complex identity technology is not currently applied to B2B use cases, as it lacks native buying group scoring and third-party data collaboration capabilities, limiting its value to B2B buyers.

BlueConic

BlueConic is positioned as a Niche Player in this Magic Quadrant. Its CDP focuses on providing marketing-first functionality to intelligently orchestrate customer touchpoints and next-best-actions (NBAs) based on unified zero- and first-party customer data. The company’s operations are typically focused in North America and Europe, and its clients generally tend to be midsize and enterprise B2C organizations across the retail, e-commerce, media and publishing verticals.

Future plans include investments in data interoperability, specifically to support zero-copy through Databricks Delta Sharing. It also plans to launch an AI shopping assistant that transforms brand sites into conversational shopping experiences.

Strengths

-

Personalization and NBA: BlueConic stands out in the market for its consistent focus on providing deep marketing functionality in its CDP. Recent investments in NBA decisioning enable the platform to leverage predictive algorithms and GenAI to evaluate profiles, behaviors and context to recommend the most relevant offer or message.

-

Use case packaging**:** In response to market demand for faster deployment and time to value, BlueConic launched several “growth plays” for customers, which are preconfigured, outcome-driven solution bundles designed to solve specific business problems such as lead generation, cart abandonment and product discovery. This approach enables customers to realize value from their investments more readily, rather than requiring a full-platform implementation.

-

Upstream privacy enforcement**:** BlueConic enforces consent upstream at the data collection point, rather than just at the activation stage. This architecture is particularly strong for AI governance because it ensures AI agents and models are prevented from inadvertently training on or utilizing nonconsented data.

Cautions

-

Overall viability: BlueConic’s growth velocity is modest, having added the fewest new customers in 2024 of vendors in this evaluation and is projecting to add the fewest in 2025. The company has undergone significant leadership changes, including a new CEO in early 2025, as well as multiple reductions in its workforce.

-

Zero-copy data sharing: BlueConic only supports zero-copy data sharing with one cloud data warehouse partner (Snowflake), which is more limited than any other vendor in this evaluation. Given the increasing demand for data interoperability in this market, buyers should carefully consider whether BlueConic and its roadmap can support their organization’s enterprise data requirements.

-

B2B capabilities: BlueConic lacks support for some key B2B functions, such as the discovery and mapping of buying team members. As the expected scope of CDPs expands to encompass broader unified commercial motions and back office use cases, buyers should assess to what degree they would require a custom implementation to meet requirements.

Hightouch

Hightouch is positioned as a Leader in this Magic Quadrant. Its modular platform — comprising Customer Studio, Hightouch Agents, Hightouch Events, Match Booster, AI Decisioning and Reverse ETL — enables collection, management and activation of customer data directly to or from an organization’s data warehouse or lakehouse. Hightouch primarily operates in North America and Europe, serving B2C clients in sectors such as retail, media, travel and hospitality.

Future plans emphasize agentic AI for outcome-based marketing, automated content generation and enhanced enterprise data fabric support.

Strengths

-

Composable architecture leadership: Hightouch was among the first to advance warehouse-native CDPs, activating data directly from clients’ existing infrastructures (e.g., Snowflake, Databricks). This eliminates replication latency and costs, helping customers leverage their data fabric for activation and building Hightouch’s strong brand reputation.

-

Agentic AI vision: Hightouch seeks to replace traditional marketing workflows with always-on AI agents that pursue marketer-defined goals (e.g., “drive second purchase”). Its AI Decisioning module uses outcome-based algorithms to autonomously personalize and optimize content, timing and channels, shifting marketers from episodic campaigns to continuous journey optimization.

-

Advertising support: Hightouch stands out for deep advertising ecosystem integrations, including connected TV and retail media networks. Its Match Booster module enriches customer data in-flight with third-party identifiers, improving match rates and addressability across major ad platforms.

Cautions

-

Buyer alignment: Hightouch’s warehouse-native architecture positions data engineering work as the customer’s responsibility, and its roadmap emphasizes marketing-focused capabilities (journey orchestration, AI decisioning, content generation). This approach is a strategic fit for organizations with mature data ecosystems and strong data teams willing to own modeling and transformation rather than delegating it to the CDP vendor.

-

Vertical concentration and B2B maturity: Hightouch’s client base is concentrated in retail, high tech and fintech, with limited presence in regulated industries, such as traditional financial services and pharmaceuticals. While Hightouch does serve B2B clients, the platform is less suitable for complex B2B orchestration due to modest support for features like buying group discovery.

-

Ecosystem and geographic limitations: Hightouch’s growth relies heavily on major data warehouse partners, lacking the broader independent software vendor networks of larger competitors. Geographic support is limited; North America and Europe have local teams, while other regions are served by third-party resellers, which may constrain adoption for global enterprises.

Oracle

Oracle is positioned as a Leader in this Magic Quadrant. Its solution, Oracle Fusion Unity Data Platform, enables large B2B and B2C enterprises with complex data management needs to deliver unified customer experiences (CXs) while connecting back-office and commercial business processes to accelerate revenue. Its geographically diverse operations serve enterprises across multiple sectors.

Future plans include additional investments in GenAI and AI agent workflows to support broader use cases beyond traditional marketing activation such as data assessment agents and product fit scoring. Additional plans include a new data orchestration canvas and stronger interoperability and zero-copy data sharing with external data warehouses.

Strengths

-

B2B ecosystem focus**:** Oracle unifies customer, account and B2B commercial data from ERP, supply chain, HR, sales and service in one place. By embedding the Oracle Fusion Unity Data Platform into the Oracle Fusion Applications framework, Oracle helps its enterprise installed base accelerate time to value of real-time, front-to-back-office AI use cases.

-

Embedded AI Studio and workflows: Oracle Fusion AI Agent Studio, included in the base CDP offering and Oracle Fusion Applications framework, provides a unique canvas-based UI for building, connecting and governing GenAI and agentic processes, enabling orchestration of full-stack, cross-functional commercial customer data AI decisioning workflows and experiences.

-

Flexible entity mastering: Oracle handles complex organizational data across multiple data object levels, including customers, accounts, households, products and locations. Advanced features go beyond basic profiles to include visual account views, AI-based buying group modeling and scoring and automated job title normalization.

Cautions

-

Pricing visibility: Oracle does not charge for features such as data ingress/egress or building and running AI agents in the AI Agent Studio; however, overall costs are unclear, as a sample proposal provided for this evaluation lacked sufficient detail to break down SKU-level pricing levers or metering conditions that would aid in forecasting TCO. Customers should note that external data warehouse vendors may charge for queries or data transfer, and building and running custom agents could incur additional, less predictable charges.

-

Data clean room support: While it integrates with third-party data providers for enrichment, including ZoomInfo, Dun & Bradstreet, LiveRamp and Acxiom, Oracle relies on partners to support data clean room capabilities rather than offering them natively.

-

Nontechnical buyer focus: Although Oracle offers advanced tools such as the Intelligence Workbench, self-reported metrics reveal that only 10% of its users are technical, with data architects and analytics personnel making up just 7%, suggesting a disconnect between Oracle’s messaging and technical adoption. Buyers with strong analytics or business intelligence needs should carefully consider their use cases and the level of granularity available in technical data and analytics controls.

Salesforce

Salesforce is positioned as a Leader in this Magic Quadrant. Its solution, Data 360 (formerly Data Cloud), serves as its platform’s CDP, with broad use case support across marketing, service, sales, commerce and analytics. Salesforce serves enterprises globally across a range of business models and industries, including financial services, retail, media and manufacturing.

Future plans include adding capabilities to its Data 360 Clean Room, which supports privacy-safe data collaboration using a zero-copy network. It is also investing in agentic innovations such as agentic enterprise search and context agentic memory, which aim to bring together short-term interactions and long-term knowledge for AI agents to have holistic situational understanding.

Strengths

-

Innovative vision: Salesforce is positioning Data 360 as the context engine for unifying structured and unstructured data across multimodal content, accessible to any agent in real time. Customers requiring support for end-to-end CX and complex back-office use cases may benefit from a CDP vision that is broader than most vendors in this market, a capability bolstered by its recent acquisition of Informatica.

-

Market traction: Salesforce reported a 141% year-over-year growth in paying Data 360 customers in fiscal 3Q26. Furthermore, Salesforce was listed as a top competitor for its CDP offering by every participating vendor in this evaluation.

-

Customer success: Data 360 offers three tiers of customer success plans, ranging from the free learning platform, to Trailhead, to hands-on workshops and highly personalized architecture guidance for an additional cost. The Datablazer community comprises more than 70,000 members, and there are more than 2.4 million certified Data 360 badges on Trailhead.

Cautions

-

Pricing model complexity: Unpredictable credit consumption is a consistent challenge, with some Gartner clients reporting exhausted credit limits without delivering value. Salesforce’s digital wallet has alleviated some of the credit uncertainty by allowing users to track credit consumption. However, it doesn’t yet enable forward-looking spend forecasting, making it difficult for users to plan their use cases and budget appropriately.

-

Ecosystem dependency: Organizations with diverse, non-Salesforce tech stacks may find the platform’s value harder to realize, as the capabilities of Data 360 are most powerful when deeply integrated with other Salesforce Clouds and products. To scale capabilities, clients may be required to license additional products, such as Marketing Intelligence and Tableau for analytical use cases.

-

Sales execution: Some Gartner clients, particularly those in IT, report limited awareness of Data 360’s capabilities and its positioning as a CDP offering. Furthermore, there is market confusion regarding the necessity of Data 360 to scale Agentforce, raising concerns about Salesforce’s ability to connect sales execution to value realization for customers who may not be aware of the product’s use cases and limitations.

Tealium

Tealium is positioned as a Challenger in this Magic Quadrant. The Tealium Customer Data Hub offers a full CDP solution, while Tealium Collect is its composable CDP. With over 1,200 prebuilt integrations, Tealium offers a user-friendly interface with low- and no-code features, broad use case support and a visual debugger. A global company, its operations are typically focused in North America and Europe, and its clients generally tend to be large B2C and B2B enterprises across sectors like banking, financial services and retail.

Future plans include advancing the platform’s agentic AI features with conversational interfaces, bolstering autonomous data quality monitoring and building better customer understanding with intelligent orchestration.

Strengths

-

Partner program: Tealium’s structured partner certification program features defined tiers and requires hands-on practical assessments, with Implementation Certifications valid for 36 months to ensure partner expertise. Additionally, Tealium offers an expanded suite of learning resources — available on-demand, virtually and in-person — at no cost to partners.

-

Extensive integration ecosystem: Tealium’s expansive network of real-time integrations are engineered to optimize for individual vendor APIs, offering a robust integration framework that enables the platform to trigger direct actions and workflows, extending well beyond basic data synchronization.

-

Specialized vertical offerings: Tealium supports highly regulated industries through Health Insurance Portability and Accountability Act (HIPAA)-compliant private cloud environments and dedicated pharmaceutical and healthcare sector product bundles. It also offers specialized integrations with industry-specific technologies, such as Veeva and IQVIA for pharmaceuticals and CDK, DealerTrack and CallRevu for automotive dealer management.

Cautions

-

Decelerating market momentum and revenue growth: Tealium is experiencing a slowdown in market velocity and diminished customer acquisition, evidenced by a decline in its annual recurring revenue growth rate from 2021 to 2025. Buyers evaluating technology for their long-term roadmaps should consider whether Tealium is an appropriate fit, particularly given recent declines in total customer count.

-

Innovation and feature development: Tealium’s investments in emerging technologies and innovation remain behind market expectations, with recent developments more focused on closing competitive gaps rather than establishing market leadership. Customers should assess whether Tealium’s current innovation and roadmap meets their long-term needs.

-

Event-based pricing: Tealium’s core pricing model is based on ingested data event volume, which can lead to unpredictable costs for use cases involving real-time, interactive or agentic applications. Customers deploying highly interactive solutions, such as conversational interfaces or real-time personalization, may generate substantially higher costs compared to traditional, static marketing campaigns.

Treasure Data

Treasure Data is positioned as a Challenger in this Magic Quadrant. Its Intelligent CDP focuses on unifying customer data via its Diamond Record universal ID and enables flexible activation through a Hybrid CDP architecture that supports packaged and composable deployments. The company’s operations are focused in North America, EMEA and APAC, and its clients generally tend to be large B2C and B2B enterprises across sectors such as retail, consumer products and automotive.

Future plans are focused on agentic process optimization, including expanding its journey orchestration and coordination capabilities, such as an autonomous Marketing Super Agent.

Strengths

-

Data interoperability: Treasure Data’s Hybrid CDP model supports Complete Mode (CDP as the source of truth) and Composable Mode (cloud-based data warehouse as the source of truth). Zero-copy integration with platforms such as Snowflake and Databricks allows enterprises to query, process and activate data where it resides, maximizing adaptability to individual data environments.

-

Real-time decisioning and orchestration: The platform delivers subsecond latency for profile lookups and decisioning, enabling brands to respond to customer signals within a single interaction window. Its customer journey orchestration tools leverage these real-time signals to automate multistep, cross-channel campaigns, dynamically adjusting content and offers based on behavioral data.

-

Agentic AI innovation**:** Treasure Data is aggressively expanding its AI capabilities through its AI Agent Foundry, a framework for building and deploying autonomous agents for audience discovery, reporting and journey optimization. While GenAI assistant and copilot are standard in CDPs, Treasure Data’s agentic focus differentiates it by betting on an agentic martech future, where specialized agents collaborate to drive marketing outcomes and operational efficiency as an alternative to EAPs.

Cautions

-

Pricing and retention metrics: Treasure Data’s updated pricing model is driven by customer profiles, events, orchestration actions and credits for its AI suites, such as Personalization AI, which orchestrates real-time web interactions. While scalable, costs can increase rapidly as usage grows. Treasure Data’s response to a sample pricing scenario for this evaluation was nearly double that of the second highest response and four times the average across all vendors. Clients should diligently confirm positive business benefits and mitigate overlap with other personalization and multichannel marketing technologies in use.

-

Technology partner competition**:** Treasure Data’s goal of becoming a Marketing Superagent risks diluting its core identity as a CDP. This strategy places Treasure Data in direct competition with its own martech partners, creating channel conflict that may disincentivize the ecosystem it relies on for channel-agnostic activation.

-

Midmarket ambitions: Treasure Data signaled an intent to expand into the upper midmarket segment, with new rate cards and accelerators for organizations with $500 million to $1 billion in revenue. Midmarket buyers should ensure they have a comprehensive understanding of how pricing structures for profile and behavioral data consumption, AI suite credits and associated service fees are aligned with their anticipated path to value realization.

Twilio

Twilio is positioned as a Niche Player in this Magic Quadrant. Its Twilio Segment CDP (which comprises modules such as Twilio Segment Connections, Twilio Unify and Twilio Engage Foundations), focuses on operating as a composable CDP that emphasizes modular components and provides granular data management and profile unification controls. Its operations are focused in North America, EMEA and APAC, and its clients tend to be large enterprises across sectors such as B2B tech, retail, e-commerce, financial services and health/life sciences.

Future plans include integrating more AI/ML features, privacy and data governance enhancements and deeper integration with Twilio’s communications products as part of its Customer Engagement Platform strategy to enable personalized omni-channel customer journey orchestration using real-time data.

Twilio declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

Strengths

-

Privacy and governance: Segment CDP integrates with consent and preference management platforms, such as OneTrust, and enforces compliance with GDPR, CCPA and HIPAA. Its Privacy Portal streamlines privacy with real-time automated identification and classification of personal data, including PII and PHI. Schema controls allow selective blocking or omission of properties during streaming, supporting a single source of truth and tracking plan for collected customer events and properties.

-

Data interoperability: Segment CDP features a flexible, open ecosystem with more than 700 prebuilt connectors. Its Functions Copilot includes over 5,700 custom functions to help accelerate data management integrations for customers, and Twilio embraced interoperability with a Linked Audiences tool for marketers to directly query and segment in a data warehouse using a no-code interface.

-

Developer and tech user experience (UX): Twilio continues to invest in making Segment more developer friendly with improved APIs, software development kits and tools for custom integrations and data pipelines. The platform’s granular data management and profile unification controls are highly beneficial for technical marketing teams.

Cautions

-

B2B experience management: Segment lacks extensive B2B-focused account traits in its out-of-the-box data graph and offers only limited account hierarchy management, requiring customized solutions or APIs to deploy robust B2B features, rather than relying on native support.

-

Stand-alone CDP innovation**:** Twilio’s focus on supporting its communications platform as a service creates uncertainty regarding the development of its CDP offering, particularly following the planned sunset of Twilio Engage Premier, announced in June 2025. This strategic pivot raises concerns regarding Twilio’s long-term commitment to CDP innovation and stand-alone orchestration capabilities.

-

Measurement and reporting: Limitations in Segment’s native performance reporting and integrated ROI tracking can present organizational challenges for customers trying to quantify and justify the value of their CDP investment to executive leadership.

Uniphore

Uniphore is positioned as a Leader in this Magic Quadrant. Its solution, Uniphore Marketing AI (formerly ActionIQ) features a universal data architecture with federated, zero-copy data sharing capabilities and robust integrations with major enterprise data warehouses. The platform supports marketing technology (martech) and IT leads with hybrid composable approaches to curate and virtualize datasets. Its U.S.-based operations mostly serve B2C and B2B clients in media, retail, financial services and high tech.

Future plans include investments in agentic identity resolution, unified knowledge layers for campaign intelligence and expanded full support for unstructured data.

Strengths

-

Enterprise data strategy: Uniphore adopts a comprehensive approach to CDP technology, positioning it as an intelligent data fabric with warehouse-native architecture and zero-copy querying that enable activation without data replication across all major cloud data warehouse vendors. The platform’s hybrid composable model supports structured, semistructured and unstructured data, facilitating governed, real-time, AI-augmented activation.

-

Granular control of segmentation: Uniphore calculates segments at runtime, triggered by user actions or new data inputs, with no limitations on the number of segments or refresh frequency. The platform also leverages LLMs to deliver a prompt-based UX for segmentation, which requires additional compute resources but does not factor into Uniphore’s pricing.

-

Integration ecosystem: The platform provides robust connectivity across the enterprise technology stack. This includes bidirectional, prebuilt integrations with some CRM, ERP and call/contact center solutions.

Cautions

-

Strategic direction: Uniphore’s acquisition of ActionIQ in late 2024 has introduced uncertainty regarding how its CDP functionally aligns with its broader Business AI Cloud platform. Prospective buyers should ensure that Uniphore Marketing AI’s current capabilities and roadmap support their long-term CDP objectives.

-

Product roadmap: Although the platform features an ambitious roadmap, recent innovations and planned enhancements are primarily focused on advertising use cases, which diverges from its historical emphasis on data management. Campaign planning, agentic identity resolution and audience building are important to a subset of buyers, and those pursuing these features may risk feature duplication with other solutions in their tech stack as the CDP category continues its consolidation and maturation.

-

Technical user dependencies: Platform adoption remains highly dependent on specialized technical roles, with martech and IT leads, as well as data architects and engineers as the core user group, which contrasts with the predominantly nontechnical user base. Buyers should verify that their internal teams possess the requisite technical expertise to deploy and manage the platform on an ongoing basis.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

- Hightouch was added to this year’s evaluation.

Dropped

-

Redpoint Global offers its Redpoint CDP, which emphasizes upstream data quality, automating data cleansing and identity resolution to provide AI-ready data for personalization and campaign orchestration. It was not included because the product did not meet the inclusion criteria for CDP software customers and contract value.

-

Rokt mParticle offers a CDP focused on analyzing, activating and governing audience data to support life cycle marketing for B2C brands. It was not included because the product did not meet the inclusion criteria for CDP software customers and contract value.

-

Zeta Global delivers data management, segmentation, personalization and omnichannel activation through its Zeta Marketing Platform. The product did not meet the minimum requirements for CDP software customers and contract value in this year’s inclusion criteria.

Inclusion and Exclusion Criteria

To qualify for inclusion, providers need to satisfy the following criteria:

1.0 Alignment With Market Definition

-

1.1 Functionality: CDPs must align with the Market Definition. The modules submitted as the base CDP software offering (single product license [SKU] or bundle of product licenses) must, at a minimum, compose a solution that performs the basic functionality outlined in the Market Definition.

-

1.2 General availability: CDP products must be generally available as of 1 September 2025. General availability is defined as something a vendor’s clients have in a production environment, rather than something they are testing or evaluating.

2.0 Business/Financial Performance

2.1 CDP software customers and contract value: The vendor is required to meet one of the following three items (in USD, reported as constant currency):

-

At least $600,000 average annual contract value (ACV)* in 2024, and

- At least 400 CDP customers** (logos) in 2024.

-

At least $250,000 ACV* in 2024, and

-

At least 250 CDP customers** (logos) in 2024, and

-

The vendor added at least 40 paying net new CDP customers*** in 2024, compared with 2023.

-

-

At least 50 CDP customers** and no more than 250 CDP customers,** and

-

An ACV* growth rate of at least 15% for all CDP customers in 2025 over 2024, and at least two CDP customers** in 2025 with annual revenue above $1 billion, and

-

At least 10 net new CDP customers*** in 2025 and at least one net new CDP customer*** in 2025 with annual revenue above $1 billion, and

-

At least $10 million in cash on hand or enough funding to survive for a year without outside financing.

-

Note: All references to “2025” as part of option 3 pertain to year-to-date numbers up to 1 September 2025.

-

2.2 Total business revenue: At least 75% of 2024 total company revenue attributable to software license sales (CDP or otherwise), either SaaS/subscription revenue or new perpetual license sales.

Definitions**: 2.0 Business/Financial Performance**

-

*Average annual contract value (ACV) must be calculated only using CDP clients.

-

**Definition of a CDP customer: A CDP customer is defined as any current licensee of the provider’s primary CDP product. To count as a CDP customer, the product must include all the necessary modules, components or bundled offerings required to meet the minimum CDP functionality criteria described above (data collection, profile unification, activation and analytic reporting). Customers using only partial or incomplete solutions that do not fulfill all these core requirements should not be counted.

-

***Definition of a net new CDP customer: A net new customer, account or logo is defined as a prospect with which the provider has not previously engaged in a commercial relationship. In other words, this is a customer that does not appear in the existing customer portfolio and represents a wholly new revenue opportunity for the provider.

-

Please note: Only count as CDP customers those organizations that have current licenses for all the modules you submit as your baseline CDP product, bundle or solution, not those using only individual modules (see 1.2 for Base Software Requirements).

Example

ModularTech offers its CDP in four separate modules:

-

Data ingestor (data collection)

-

Profile builder (profile unification)

-

Campaign activator (activation)

-

Insight analyzer (analytic reporting)

To qualify as a CDP customer, ModularTech’s client must license all four modules, either as a prepackaged bundle or as individually licensed components that together provide the full CDP functionality.

-

Counted as a CDP customer: Company A licenses all four modules.

-

Not counted as a CDP customer: Company B licenses only Data Ingestor and Profile Builder.

3.0 Licensing

**3.**1 CDP product licensing: The vendor must offer its primary CDP product as a stand-alone or base configuration (lowest edition tier) license that does not require the purchase of other independent product SKUs (excludes consumable product SKUs, see Definitions below).

Definitions

CDP product licensing: We will use the following terminology for product and licensing requirements in our inclusion criteria and throughout this research project:

-

Primary CDP product

-

Consumable product SKUs supporting the primary CDP product

-

Independent product SKUs sold in a solution with the primary CDP product

Primary CDP product: The vendor product or offering refers to the (not a suite of products) — software acquired under a single license, using the same codebase and repository, not requiring any customized integration to access and exchange data.

This product’s license provides access to the foundational CDP application as well as all essential and some advanced CDP functionality, as described below. CDP primary product licenses exist in one of two forms:

-

Application or platform license: Grants access to essential CDP features, such as audience segmentation, data orchestration and analytics.

-

Edition-based application or platform license: These tiered pricing models offer different levels of access to CDP features, pricing and supporting consumables (e.g., Essentials, Professional and Enterprise).

Consumable Product SKUs Supporting the Primary CDP Product

-

Data or computational units: Credits, tokens or other variable data storage, data processing, segmentation and personalization. Examples include:

-

Contact, profile or user volumes, such as monthly active or monthly tracked users.

-

API calls, AI usage credits (assistants or agent), sessions, event-driven triggers, batch loads or other data processing costs (e.g., webhooks).

-

Catalogs and other data extensions that are not sold separately from the primary CDP product.

-

Consumption applicable to GenAI or agentic features for content generation, analytics, segmentation, activation, etc.

-

Prebuilt connectors: Plug-and-play integrations with other CRM, commerce, analytics or loyalty applications.

- Please note: We exclude all in-house services from the definition of a consumable supporting the primary CDP product. We define nonsoftware or services revenue as any revenue from activities related to account management, operational staff augmentation, professional or strategic services, training, implementation and onboarding. We do not distinguish between human and AI agent fulfillment models for these named services. Nonsoftware revenue may not be counted as CDP revenue.

Independent product SKUs sold in a solution with the primary CDP product:

A provider’s independent products extend its primary CDP product’s capabilities significantly. They operate stand-alone and as part of an integrated solution within a vendor’s ecosystem. Though they may be bundled with the CDP, independent products are licensed separately from the primary CDP product and may have distinct pricing, contracts and support terms. They are often sold to stakeholders beyond multichannel teams, such as marketing analytics, commerce or IT.

Independent products commonly sold in solution with a CDP product include, but are not limited to:

-

Multichannel marketing hubs: Includes campaign management, orchestration, multichannel execution and reporting.

-

Personalization engine: Includes content decisioning, product recommendations and behavioral targeting optimization.

-

Analytics, business intelligence or decisioning: Includes products offering predictive marketing or general analytics features. Also included are tools for model development, real-time model execution and model life cycle management.

-

Commerce platform: Systems for personalized purchase experiences, abandoned cart recovery and loyalty messaging.

-

Data products: Includes consumer segmentation, identity resolution services (deterministic or probabilistic), data clean rooms or advanced data warehousing products.

Honorable Mentions

-

Census, a Fivetran company, is a reverse ETL platform that unifies, enhances and activates data. It did not meet the inclusion criteria for this research.

-

GrowthLoop offers the Compound Marketing Engine, an agentic AI-powered composable CDP. It emphasizes interoperability with data warehouse platforms and activates to over 100 destinations. It did not meet the inclusion criteria for this research.

-

Microsoft offers Dynamics 365 Customer Insights, which is positioned as part of a suite of agentic customer experience across marketing, sales and service solutions. The tool did not meet the inclusion criteria for this research.

-

RudderStack offers its Data Cloud CDP, a composable, warehouse-centric solution for organizations seeking to collect, govern and activate their customer data from their existing data warehouse or lakehouse. The product did not meet the inclusion criteria for this research.

Evaluation Criteria

Ability to Execute

Gartner analysts evaluate vendors on the quality and efficacy of the processes, systems, methods or procedures that enable a marketing team’s performance to be competitive, efficient and effective and to positively impact revenue, retention and reputation within Gartner’s view of the market. With wide-ranging functional, support and service requirements, it’s important to keep in mind the important aspects of a vendor’s Ability to Execute.

Product/Service: Core goods and services that compete in and or serve the defined market. This includes current product and service capabilities, quality, feature sets, skills and so on. This can be offered natively or through OEM agreements/partnerships as defined in the Market Definition and detailed in the subcriteria. Specifically, this evaluates the execution, delivery and usability of the functionalities noted above in the Critical Capabilities sections and each product’s alignment to the Use Cases in the Critical Capabilities.

Overall Viability: An assessment of the organization’s overall financial health as well as the financial and practical success of the business unit. It also includes the likelihood of the organization to continue to offer and invest in the product as well as the product position in the current portfolio. Specifically, we examine evidence of profitability and growth, customer growth and retention and R&D investment as well as alignment and levels of current and planned organizational resources.

Sales Execution/Pricing: The organization’s capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support and the overall effectiveness of the sales channel. Specifically, we examine the vendor’s ability to provide clear, transparent and flexible pricing models as well as the availability of tools or processes that support clients in forecasting their usage across business scenarios and measuring ROI. We assess the vendor’s pricing models and how they align with their target ICPs’ operating model; how the vendor derives value both internally and through its customers; the vendor’s understanding of typical implementation approaches; and the availability of assessments and POCs.

Market Responsiveness and Track Record: The ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the provider’s history of responsiveness to changing market demands. Specifically, we assess how each vendor responds to rapid market shifts. This includes how the vendor considers customer needs in developing product updates and the vendor’s approach to customer success programs.

Marketing Execution: Not evaluated.

Customer Experience: Products and services and/or programs that enable customers to achieve anticipated results with the products evaluated. This includes quality supplier/buyer interactions, technical support and account support. This may also include ancillary tools, customer support programs, the availability of user groups, service-level agreements, etc. Specifically, we assess client satisfaction; information on technical support and implementation; user interface(s) that support target user roles; availability and viability of internal customer service and support capabilities; the vendor’s approach to facilitating clients’ smooth implementation and adoption of its CDP; and the vendor’s clients’ ability to deliver measurable ROI on their technology investment.

Operations: The ability of the organization to meet goals and commitments. Factors include quality of the organizational structure, skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently. Specifically, we assess the operational health and ability to deliver for customers consistently and efficiently, whether directly and/or through partners (including via professional services). We also examine the relevance of the vendor’s operations (e.g., technology partners, partner networks and integrations) to the enterprise buyer.

Ability to Execute Evaluation Criteria

| Product or Service | High |

| Overall Viability | Medium |

| Sales Execution/Pricing | High |

| Market Responsiveness/Record | Medium |

| Marketing Execution | NotRated |

| Customer Experience | High |

| Operations | Medium |

Source: Gartner (January 2026)

Completeness of Vision

Gartner analysts evaluate providers on their ability to convincingly articulate logical statements. This includes current and future market direction, innovation, customer needs and competitive forces. It also includes how well they map to Gartner’s view of the market.

Market Understanding: The ability to understand customer needs and translate them into products and services. Vendors that show a clear vision of their market; they listen, understand customer demands and can shape or enhance market changes with their added vision. Specifically, we assess the understanding of how the CDP fits into a broader enterprise data ecosystem. We examine how the CDP helps clients evaluate its cost to value, the approach to composable architectures and data interoperability (how it will enhance CDPs to operate effectively within a client’s larger data architecture) and how the vendor demonstrates a grasp of existing and emerging business use cases and aligns them to product and go-to-market (GTM) investment priorities.

Marketing Strategy: Clear, differentiated messaging consistently communicated internally, and externalized through social media, advertising, customer programs and positioning statements. Specifically, we look for evidence that the marketing strategy supports the CDP’s target markets and customer personas. This includes evidence of buyer support, enablement and advocacy, including tools that support buying, adoption, retention and value expression of the CDP.

Sales Strategy: A sound strategy for selling that uses the appropriate networks, including direct and indirect sales, marketing, service and communication. Partners that extend the scope and depth of market reach, expertise, technologies, services and their customer base. Specifically, we evaluate how the vendor clearly and thoughtfully defines its ideal customer profiles and target market segments. We examine each vendor’s plans to demonstrate long-term focus on its market position, especially in a market where cross-functional buying groups have become the norm. We also examine the effectiveness of the partner network in extending market reach and supporting complex, enterprise-level implementations

Offering (Product) Strategy: An approach to product development and delivery that emphasizes market differentiation, functionality, methodology and features as they map to current and future requirements. Specifically, we assess the product roadmap, including its focus on seamless integration with broader enterprise data ecosystems (e.g., cloud data warehouses, data lakes, data fabrics), the plan to develop advanced AI/ML capabilities (including agentic AI) to support a wide range of use cases across business functions and the clarity of product packaging.

Business Model: The design, logic and execution of the organization’s business proposition to achieve continued success. Specifically, we assess the significance of the CDP product to the vendor’s overall business and any key partnerships or divestitures the vendor makes. We examine the alignment of each vendor’s go-to-market and sales strategies for particular industries, geographies and delivery models. We also look at how the product strategy supports the business model as well as how the product license model (for example, SaaS versus a one-time license fee) effectively supports a vendor’s targeted market.

Vertical/Industry Strategy: The strategy to direct resources (sales, product, development), skills and products to meet the specific needs of individual market segments, including verticals. Specifically, we gather information regarding vertical- and industry-specific product roadmaps/partnerships.

Innovation: Marshaling of resources, expertise or capital for competitive advantage, investment, consolidation or defense against acquisition. Specifically, we assess each vendor’s outlook toward innovation for differentiation, appropriate M&A exploration and execution, development plans and alignment of those plans with newer technologies coming to the market (e.g., agentic AI, data sharing technologies, composable architectures and converged data management platforms/data ecosystem approaches).

Geographic Strategy: The provider’s strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the home or native geography, either directly or through partners, channels and subsidiaries, as appropriate for that geography and market. Specifically, we look for any region-specific partnerships to support locations and product capabilities that meet unique customer needs in various regions (e.g., data residency requirements, language localization and geographic specificity of partners).

Completeness of Vision Evaluation Criteria

| Market Understanding | High |

| Marketing Strategy | Low |

| Sales Strategy | Low |

| Offering (Product) Strategy | High |

| Business Model | Medium |

| Vertical/Industry Strategy | Medium |

| Innovation | High |

| Geographic Strategy | Low |

Source: Gartner (January 2026)

Quadrant Descriptions

Leaders

Leaders in this market demonstrate strong execution on current market needs while maintaining a compelling vision for the future, establishing themselves as the governed, flexible execution layer for the enterprise AI ecosystem. These providers generally excel in one of the two major market paradigms: platformization or agentification. Leaders focusing on platformization (such as those from enterprise application platforms) provide broad, cross-functional orchestration capabilities, embedding AI agents and unifying operational and customer data to serve complex B2B and enterprise data needs. Other Leaders may focus on leading the composable architecture trend, activating data directly from clients’ existing data warehouses or lakehouses, while pursuing aggressive visions for autonomous agentic AI to replace traditional marketing workflows. Leaders support the expanded, enterprisewide scope of the CDP, which now serves as an intelligent data fabric and context engine.

Challengers

Challengers in this market exhibit high execution capabilities, often possessing strong traction through robust ecosystem integrations, sophisticated architectural models or specialized vertical offerings. Providers in this quadrant typically offer full CDP solutions or flexible, hybrid architectures that support composable deployments, delivering capabilities like real-time decisioning and orchestration with subsecond latency. However, their overall market vision or long-term momentum may trail the Leaders. They may face organizational headwinds, such as decelerating market velocity or diminished customer acquisition, or they focus their innovation efforts on closing competitive gaps, rather than setting market direction. Some Challengers are aggressively pivoting toward an agentic AI future, betting that autonomous agents can transform their platform into a comprehensive marketing engine, but this approach may risk diluting their core CDP identity

Visionaries

A typical Visionary in the CDP market demonstrates a deep understanding of current and future customer needs and articulates a clear vision for innovation, but their Ability to Execute may be limited in scope or market reach. These providers possess specialized strengths, such as exceptional real-time data management via distributed edge networks or pioneering efforts in privacy-centric data collaboration and clean-room applications. Visionaries provide solutions with out-of-the-box data models and schemas to support complex global enterprises in specific verticals. However, their utility might be concentrated in specific use cases, such as B2C marketing, rather than providing the broad enterprise data management capabilities sought by IT and data operations buyers. Visionaries may also lag in the maturity of their composability and warehouse interoperability compared to independent competitors

Niche Players

Niche Players in the CDP market typically focus on executing well within a defined segment of the market, which may be based on functionality, geography or customer size. These providers often excel in specialized areas, such as solving complex identity resolution challenges, emphasizing upstream data quality and automated data cleansing, or focusing intensely on marketing-first functionality like personalization and next-best-action decisioning. Niche Players often offer significant strengths in specific areas like privacy and governance controls, or provide developer-friendly user experiences and extensive prebuilt connectors. Constraints for Niche Players often include a narrow vision (such as limited support for B2B features or data collaboration), geographical limitations or lagging innovation in key areas like agentic AI capabilities. Additionally, some Niche Players may exhibit overall viability concerns or have limited support for essential market features, such as zero-copy data sharing with major cloud data warehouses.

Context

Do You Need a Customer Data Platform — or a Customer Data Agent?

Today’s CDP market is increasingly defined by a bifurcation between two strategic paradigms: platformization and agentification.

Platformization refers to the architectural and commercial strategy where the CDP is positioned as the foundational layer of a broader, integrated application ecosystem. In this model, the CDP is not merely a stand-alone application, but rather serves as the core data capability upon which higher-order applications are built and executed natively. This includes enterprise application platforms (EAPs) from Adobe, Oracle and Salesforce. For example, Salesforce Marketing Cloud (SFMC) Next exemplifies this approach, where advanced marketing applications are rewritten to leverage the native capabilities of the underlying CDP, Data 360. Within this approach, the CDP becomes a critical module in a unified platform, and access to next-generation functionalities (e.g., agent-based automation or advanced analytics) is gated through the CDP.

The value proposition here is clear: buyers must first adopt the CDP to unlock the full suite of platform capabilities, ensuring data consistency, governance and extensibility across all applications. The value proposition is grounded in mutual dependence: buyers adopt the CDP to access next-generation platform capabilities, while vendors gain the data foundation required to deliver advanced functionality like agent-based automation and cross-functional orchestration. This dependency reflects platform architecture rather than artificial bundling — the CDP must exist as the unified data layer for higher-order applications to function as designed.

Platformization enables enterprise orchestration_._ This approach establishes shared customer data objects accessible across the platform’s application suite. This architectural consistency ensures that when a consent preference updates in one module, that change immediately constrains available actions across all customer touchpoints, preventing the compliance drift that plagues point-solution stacks.

Beyond data consistency, platformization amplifies orchestration value into cross-functional workflows (e.g., marketing-sales handoffs to a service case creation triggered by a campaign engagement). Stand-alone, composable or warehouse-native CDPs lack the deep application integration required to support these coordinated commercial motions where profile updates, preference changes and engagement signals must propagate in real time across marketing, sales, customer success and service teams. While these solutions offer API connectivity to downstream applications, they cannot enforce real-time consent propagation, cross-application profile locking during transactions or synchronized next-best-action decisioning across multiple touchpoints — capabilities that require native platform integration.

Regulated industries (e.g., banking and financial services, healthcare and pharmaceuticals) benefit from platformization through coordinated go-to-market execution with enforced consent management and compliance requirements that data warehouses don’t address. Moreover, CDPs from enterprise application platforms (EAPs) typically possess a more mature industry-specific strategy, which has proven particularly effective in attracting healthcare and financial services organizations requiring next best actions across customer-facing functions.

Agentification positions the CDP as an initial entry point that enables disruptive expansion through autonomous agents operating on the CDP’s unified profile and orchestration infrastructure. Rather than building comprehensive application suite capabilities upfront, this approach treats the CDP (or any composable martech) as the minimal viable platform for unified customer profiles and orchestration infrastructure. It then relies on specialized AI agents, operating on that foundation, for marketing execution.

This strategy resurrects the Smart Hub vision from 2020 to 2022, where some CDPs attempted to displace MMH, B2B Marketing Automation Platforms and other tools from journey orchestration. That vision failed because CDPs lacked the native execution capabilities that marketing teams required for day-to-day operations, such as email rendering, push notification infrastructure and A/B testing frameworks The 2025 version of this strategy addresses these gaps by positioning autonomous AI agents as the execution layer, all while using existing channel infrastructure while adding real-time intelligence. Still, this is very much a visionary direction and is currently better reflected in vendors’ product roadmaps and recently launched features.

Vendors like Hightouch and Treasure Data, among others, are betting that autonomous agents for content generation, next-best-action decisioning and channel optimization can transmute a CDP into a full-blown marketing platform without requiring a large investment in the massive application portfolio of Adobe or Salesforce. The value proposition shifts from a modular “composable data layer” to an “autonomous marketing engine.” The CDP establishes unified profiles and real-time decisioning APIs, and then AI agents handle everything from journey design to creative optimization to budget allocation. These providers envision that a future MarTech stack will amount to “warehouse + CDP + agents” rather than “warehouse + 50 specialized applications.”

The agentification approach also represents an innovation velocity bet: as agentic AI technology evolves rapidly, vendors following this path can potentially deploy new autonomous capabilities faster than platform vendors constrained by the need to maintain compatibility across extensive application suites. However, this advantage depends on whether autonomous agents can reliably replace the specialized functionality of established marketing, sales and service applications: a question that remains unresolved at the time of publication.

Agentification represents operational autonomy. Organizations with mature data infrastructure and high marketing velocity can deploy autonomous AI agents embedded within their CDP to execute journey orchestration, next-best-action decisioning and cross-channel optimization. These organizations will achieve platform-level marketing capabilities without cross-functional suite integration. This approach transforms the CDP from a passive data hub into an active customer operating system, where specialized agents handle campaign creation, audience arbitration and budget allocation tasks that traditionally required separate MMH and personalization engine licenses.

Industries with massive customer bases, many distinct brands, business units and high personalization demands (retail, travel, hospitality, CPG) benefit most from this model because autonomous agents enable distinct brands to operate with more independence than is possible in a large platform. The strategic bet is that more buyers, exhausted by sprawling application portfolios and seeking flexibility, will see agentic operations as delivering sufficient value and reliability to justify consolidating longstanding marketing applications into an AI-augmented, warehouse-native CDP.

The CDP market’s bifurcation into platformization and agentification reflects two distinct visions for the future of customer data management: one emphasizing integrated, end-to-end platforms and the other prioritizing modular, agent-driven extensibility. This divergence is reshaping vendor strategies and enterprise buying decisions, with significant implications for innovation, interoperability and long-term value creation.

Market Overview

CDPs Are Evolving Toward Agentic Customer Context Engines

The CDP market is undergoing a fundamental restructuring in 2026, transitioning from its primary focus on customer data unification across customer touchpoints, applications and data stores to becoming the context engine for how agents do their work in the modern enterprise. Today’s CDP market is increasingly defined by a bifurcation between two strategic paradigms: platformization and agentification (see the Market Context section of this Magic Quadrant).

Context engineering is the discipline of designing, managing and optimizing the information fed into GenAI models at inference time. While some industry narratives position CDPs as emerging “Context Engines,” this perspective can overlook the core operational value CDPs deliver. By strategically populating the LLM context window with relevant structured, unstructured, behavioral and operational data, CDPs can indeed enhance model accuracy and reliability, support sustained customer conversations, retain individual preferences and provide real-time information for sophisticated task execution.

However, CDPs have long enabled more familiar forms of contextual decisioning, such as next best action algorithms, journey orchestration and cross-functional customer profile distribution and activation, leveraging governed customer data objects to drive operational outcomes.

This distinction is subtle but significant: context engineering focuses on optimizing token windows for GenAI responses, whereas CDPs excel at operational orchestration and governed data activation across marketing, service, support and other business functions. Both approaches enable advanced decisioning and optimization, but they serve different purposes: one powers AI-driven responses whereas the other orchestrates enterprisewide customer experiences. As CDPs evolve into intelligent, context-rich data fabrics, their ability to bridge these paradigms will ensure scalable, production-grade customer experiences and robust decisioning capabilities.

How Do I “Right Size” My CDP Investment?

As the CDP market pivots into an AI-driven operating model, customers demand transparency and control over variable costs associated with the compute-driven pricing that emerged in the last couple years. They are also seeking visibility into the revenue these costs generate. In response, vendors have split their tooling into two complementary layers: digital wallets for cost forecasting and ROI dashboards for real-time value assessment.

Digital wallets (e.g., Salesforce’s Digital Wallet or Treasure Data’s credit monitor) currently report on current and past consumption. In the future, these capabilities need to develop and act as forecasting instruments that track consumption budgets over time, visualize credit burn rates and alert users when they approach predefined thresholds. By projecting future usage against contracted limits, digital wallets enable finance and operations teams to adjust capacity or renegotiate pricing before costs spiral out of control. Still, many of these tools are focused less on anticipating the value of the technology and instead are focused on showing the value of a single marketing activity.

Meanwhile, dashboards, reporting and embedded reporting agents (such as Treasure Data’s ROI Reporting Agent or Hightouch’s AI Decisioning Insights) serve as real-time feedback loops on performance. These tools measure lift through A/B and incrementality testing, attribution analyses and KPI tracking and link AI-driven actions to outcomes like revenue, lifetime value or conversion rates. This immediate insight helps marketing and analytics teams validate their spend, optimize campaign settings and continually refine audiences for maximum impact.

Still, some vendors buck the consumption-based pricing trend and are holding fast to charging on stable cost drivers (e.g., profiles under management), in some cases even bundling AI capabilities at no extra fee. Regardless of pricing model, the dual approach of digital wallets for forecasting and ROI dashboards for performance assessment ensures customers can rightsize CDP investments in real time, forecasting usage and justifying costs. For detailed guidance on consumption-based pricing governance, see Mastering Consumption-Based Martech.

Autonomous Decisioning: The Future of Orchestration

The role of the CDP in activation is evolving as marketing organizations begin to advance from manual channel orchestration to autonomous decisioning. Channels and campaign management represent earlier forms of decisioning where humans configured rules and scheduled delivery. Emerging autonomous systems will inherit this same activation infrastructure, but shift orchestration from human campaign managers to AI agents that assess context, evaluate treatments and trigger actions in real time through those same channels. Organizations developing autonomous decisioning capabilities now, where agents will continuously evaluate decisioning APIs, respect policy boundaries and programmatically execute through existing channel infrastructure, are building the foundations that will support future AI agent interactions. Competitive differentiation may well soon lie in optimizing decisioning quality to maximize customer value.

To thrive in this landscape, CDPs, regardless of their heritage as stand-alone, pure-play, composable CDPs or enterprise application CDPs, need to make a crucial leap and develop (or continue to develop) autonomous decisioning capabilities. AI agents will employ autonomous decisioning to assess customer context at every moment, weigh treatment options against an objective function designed to maximize net value and trigger (or withhold) actions based on real-time policy checks. They will cover consent validity, fatigue limits, cost constraints, quality thresholds and fairness rules (e.g., Hightouch’s AI Decisioning Agents). All of this happens within a governance framework that enforces safe autonomy and defines escalation paths for policy violations.